Litigators and counsel. Gain insight. Share insight.

Emerging Litigation Podcast

Technology-Assisted Review: Sara Lord Interviews Data Scientist Lenora Gray

In this episode, Sara Lord of Legal Metrics speaks with Lenora Gray of Redgrave Data about eDiscovery in the practice of litigation and how it has been transformed by technology-assisted review tools – or TAR, and how these tools work. Listen and learn more! PLUS: Watch the video for outtakes and bonus content!

Jury Selection in the Age of Conspiracy Theories and Distrust with Tara Trask

In this episode, we discuss picking juries in an age of misinformation, general distrust, tribalism, unleashed social media surfers, and unorthodox legal strategies unfolding on a daily basis with Tara Trask of Trask Consulting, jury and trial expert. Listen and learn more!

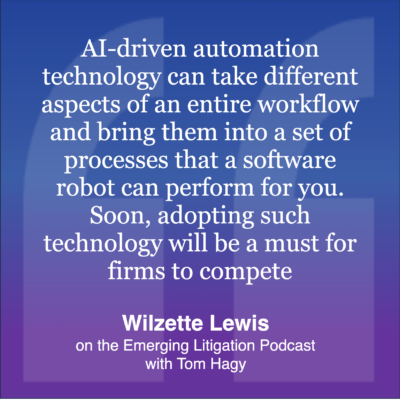

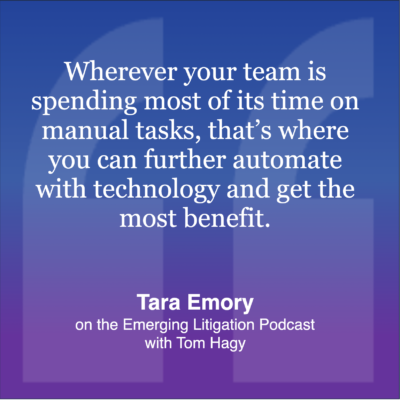

Transforming Legal Workflows with AI: Sara Lord Interviews Tara Emory and Wilzette Louis

In this episode, Sara Lord of Legal Metrics speaks with Tara Emory and Wilzette Louis of Redgrave Data about the game-changing potential of robotic process automation and AI, and how these are not just futuristic concepts but practical solutions to today's legal challenges. Listen and learn more!

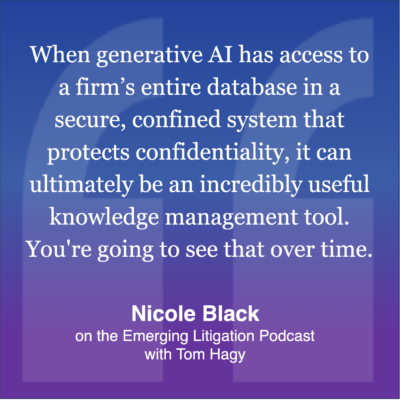

The Intersection of Generative AI and the Legal Profession with Niki Black

In this episode, we discuss the current state and future of generative artificial intelligence and the practice of law with Nicole Black, attorney, legal tech journalist, and author. Listen and learn more!

Journal on Emerging Issues in Litigation

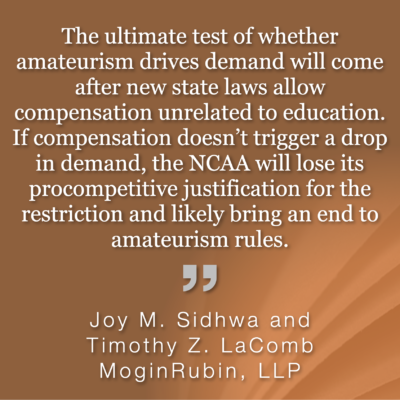

Cracking the College Sports “Cartel”: Good for Athletes, Competition, and the Games

Momentum in the national debate over whether a college athlete should profit from licensing deals for their “names, images, and likenesses,” or NILs, swung in favor of players on June 21, 2021, when the Supreme Court ruled for the athletes in NCAA v. Alston. Authors Joy Sidhwa and Tim LaComb of MoginRubin, LLP discuss the impacts of the decision and subsequent court decisions and state legislation which have further cemented and defined the changing amateurism rules in college sports.

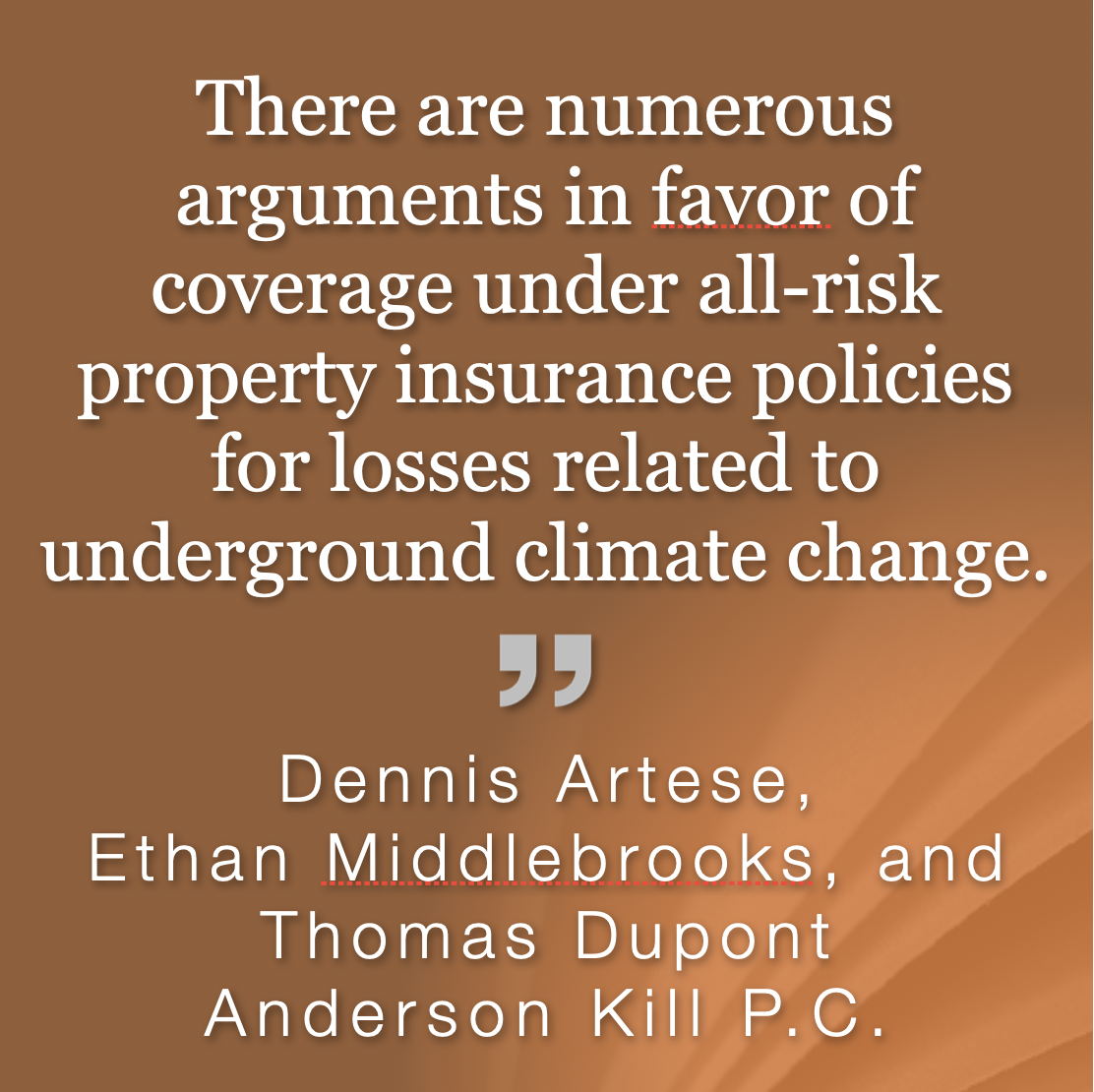

Property Insurance Coverage for Emerging Risk: Underground Climate Change

Studies have shown that “underground climate change” is affecting ground soil conditions, causing structural strains on buildings and exacerbating cracks and defects in walls and foundations. The authors, Dennis Artese, Ethan Middlebrooks, and Thomas Dupont analyze permutations of policy language and state law that may affect coverage for damage caused by underground climate change, including how state law treats anti-concurrent causation clauses, whether “human-caused” exceptions to earth movement exclusions may apply to underground climate change, and whether “abrupt collapse” exceptions to exclusions for building collapse may apply when undetected structural damage triggered by underground climate change triggers collapse.

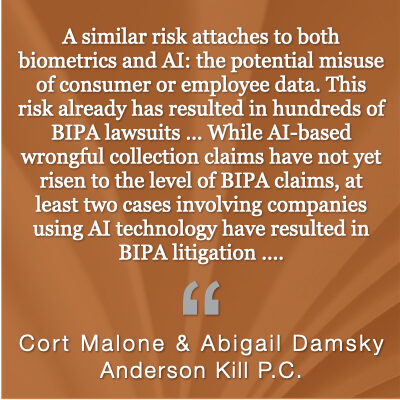

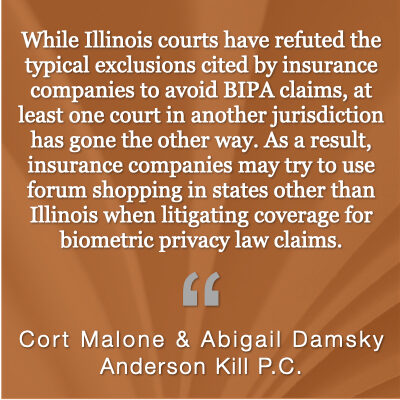

Litigation After Biometric Privacy Law Violations: Policyholder Victories and Their Implications

Insurance companies are implementing new measures to try to avoid paying for liabilities attached to consumer and employee biometric privacy law violations. The authors, Cort Malone and Abigail Damsky explore the issues companies and policyholders should be examining to ensure adequate protection in the present and future.

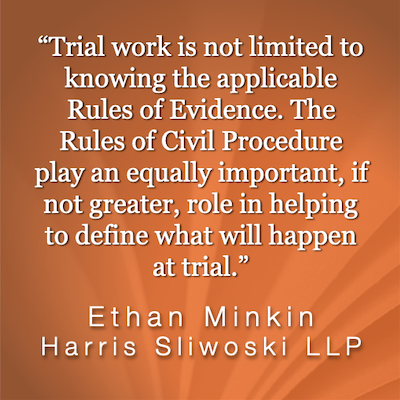

Expert Depositions and Trial Disclosures: What Every Litigator Needs to Know

Expert disclosures in litigation are vitally important for trial testimony and planning for trial. The author, Ethan Minkin examines issues surrounding expert depositions and trial disclosures, which he argues need to be appreciated to avoid unanticipated surprises at trial.

Be Our Guest

Would you like to share your insights? Contact us if you would like to be a guest on the Emerging Litigation Podcast or publish an article in the Journal of Emerging Issues in Litigation.

Write to us and take part in these exciting collaborations between HB Litigation, Critical Legal Content, vLex Fastcase, and Law Street Media.

Contact the Editor in Chief.

Partner with us to create litigation-related content that attracts eyeballs and earballs, i.e., potential clients. Don’t see a product that fits? Reach out. Let’s see what we can cook up.

Custom Work

Let us help you create branded podcasts, webinars, blogs, articles, or papers.

Publishing Services

Let us help you pitch and identify publishers for papers, commentary, analysis, practice guides, treatises, etc.

Get Featured

Appear in the Journal on Emerging Issues in Litigation or on the Emerging Litigation Podcast. Also, in some cases, we will give your existing work — articles and webinars — additional exposure on our site.

Are We a Fit?

We only take on projects if we feel we can bring value to what you do. If we don’t accept your project we will gladly refer you.

Tom Hagy

![]() Tom is HB’s Founder and Managing Director. His career in litigation content spans four decades during which he was editor, managing editor, and finally publisher at Mealey’s Litigation Reports. After Mealey’s was acquired by LexisNexis, Tom served as a vice president involved in creating new content and services at the legal research and services giant. He has always overseen or directly created articles, blogs, conferences, webinars, data collections, and now podcasts — all on litigation.

Tom is HB’s Founder and Managing Director. His career in litigation content spans four decades during which he was editor, managing editor, and finally publisher at Mealey’s Litigation Reports. After Mealey’s was acquired by LexisNexis, Tom served as a vice president involved in creating new content and services at the legal research and services giant. He has always overseen or directly created articles, blogs, conferences, webinars, data collections, and now podcasts — all on litigation.

Tom founded HB in 2008 and four years later he started Critical Legal Content, a boutique content creation shop serving specialized legal practices and litigation services. In addition to his work at HB and CLC, Tom is Editor in Chief of the Journal on Emerging Issues in Litigation, and host of the Emerging Litigation Podcast. He has served in leadership roles in publishing and content associations for which he was a frequent speaker and guest writer. Tom proudly holds a B.A. in Communications / Journalism from Bethany College in Bethany, West Virginia, and possesses some decent drumming chops.